Mezzanine Financing: An Introduction to Definition and Functionality

Mezzanine financing is an important source of funding for businesses across many industries. It exists at a “halfway” point between equity and debt, offering certain advantages (e.g. flexibility on repayment) over traditional debt and equity financing models.

While it is not widely discussed or completely understood in the mainstream yet, the importance and relevance of understanding mezzanine financing continue to rise as more companies gain exposure to the capital markets.

This blog will provide an introduction to mezzanine financing by going through its definition, functionality, pros, and cons, as well as discussing some real-world use cases where it has added value. By providing this information, readers will hopefully increase their competency with this alternative form of funding so that they can make more informed and advantageous financing decisions for their own businesses.

Contents

Mezzanine Financing

Concept of mezzanine financing

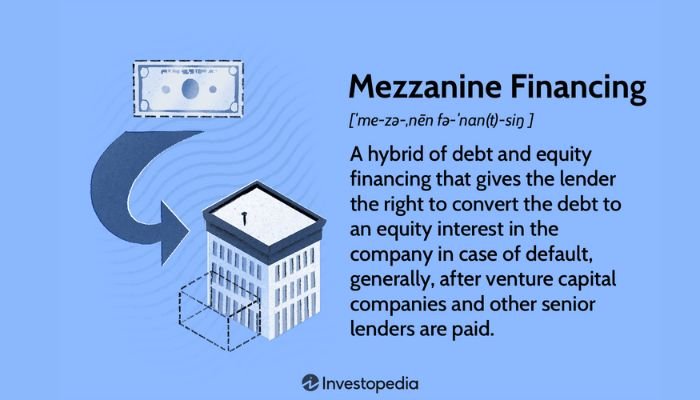

Mezzanine financing is a combination of debt and equity wherein an investor can receive both a share in the profits as well as fixed or floating payments.

It typically functions between senior debt (which has priority to be repaid first) and rigorous preferred stock that conveys certain criteria before repayment occurs.

Rich individuals, governments, private equity funds, and venture capitalists all potentially have avenues into mezzanine financing offers when looking for investments.

This form of capital grants consenting stakeholders greater flexibility regarding borrowing terms compared to bank loans used for traditional finance obtained from banks.

Differentiating mezzanine financing from other types of financing

Put simply, mezzanine financing involves an agreement between a borrower and lender where the borrower hands over part-ownership of the company in return for capital funds to fulfill its project or objectives.

Contrasting with forms of secured lending reparation such as bank overdrafts and loans, mezzanine financing is often less tightly bound to strict repayment periods or pre-executed projects which appeals to employees, directors, or shareholders who prefer nonconforming borrowing opportunities whilst also compromising some level of control in exchange for additional capital gains.

Mezzanine financing’s hybrid nature

Mezzanine financing is an attractive form of alternative financing that combines characteristics of both traditional debt and common stock. It combines the lucrative tax advantages provided by issuing company-backed debt with lower cash levies that come with equity participation from venture investors.

The hybrid nature enables borrowers to customize mezzanine financing agreements in a manner best suited for their business needs based on what lenders are willing to accept in exchange for the financial assistance capable fulfilled through the medium of these vehicles.

How Mezzanine Financing Works

Typical structure and characteristics of mezzanine financing

Mezzanine financing is a hybrid type of funding, providing capital with features of both debt and equity.

Typical structure characteristics include that mezzanine financing takes place after equity and senior debt have already been established in the “capital stack” hierarchy, it ranks higher than equity but lower than senior debt, and while providing capital allows voting rights as well as the potential to enjoy returns.

Furthermore, typical transaction terms include an interest bearing loan note plus a participation right where entities may be granted common stock or a purchase option on future sales – providing them with great leeway over any other shareholders within 90 days or more while limiting their ability to interfere in day-to-day operations.

Key stakeholders involved in mezzanine financing transactions

Mezzanine financing transactions can involve many key stakeholders, including business owners, lenders, angel investors, and private equity firms.

These parties usually enter into loan or investment agreements which will help provide capital for businesses in the event of expansion plans or general project development.

The lender provides part of the total financial requirement through traditional lending whilst the rest is provided by other sources such as institutional retrofit contribution funds, subordinated debt, and/or angel investments.

Each stakeholder brings value to the transaction based on different factors like prestige, speed of delivery, and accessible capital resources.

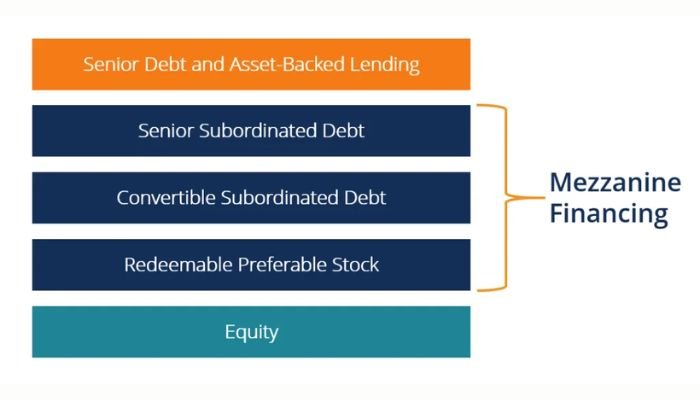

Illustration of the role of mezzanine financing in capital stack hierarchy

A mezzanine financing transaction involves different levels of debt structure based on the borrower’s operating or financial situation.

Within this “capital stack” hierarchy, junior capital such as preferred stock and subordinated debentures are typically subordinate to senior bank debt and often constitute the highest level visible tranche in related balance sheet footnotes.

Mezzanine lenders require repayment out of equity implies provided by other investors further up in the capital stack; accordingly, they institute protections in terms of baskets/exclusive events. Borrowers may also employ so-called bleed mechanisms through which operational refinancing payments filter down from their upper debt tier into more Junior Tier affiliates such as Mezzanine lenders.

Advantages and Disadvantages of Mezzanine Financing

Benefits of mezzanine financing for businesses

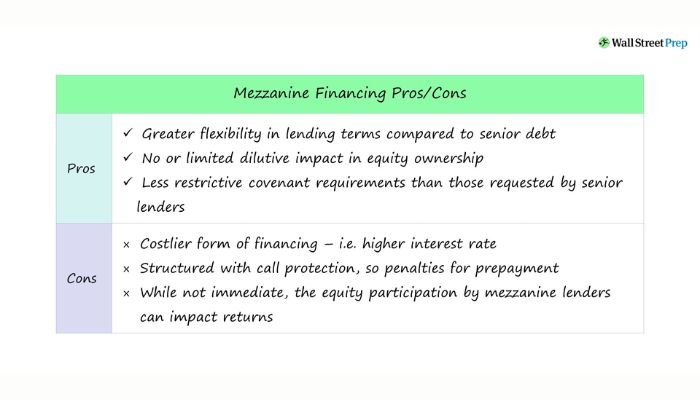

Mezzanine financing offers numerous benefits for businesses that can qualify. Its hybrid nature effectively combines debt and equity concerns to give subordinated holders a higher return rate on their investment while providing more time for borrowers to grow and repay the principal.

Further, lenders may receive tax benefit deductions, minimizing interest expenses by deducting attendant fees from business structuring or enterprise progressions. That said, those pursuing mezzanine subject to flexible but complex terms eventually risk foreclosure if unable to comply with loan amortization and payments.

Potential drawbacks or risks associated with mezzanine financing

Mezzanine financing has several potential drawbacks and risks. Most significantly, greater debt obligations can be triggered by events such as defaulting on the repayment schedule associated with the mezzanine loan.

Similarly, the issuing of warrants by lenders may alter governing share classes of equity holders and create unequal rights between lower-ranking classes and investors if interests are not aligned correctly.

Another major consideration is the cost of capital associated with obtaining a mezzanine loan – this form of lending usually comes at a favourable imposed premium regardless of economic conditions.

Conclusion

In conclusion, mezzanine financing is a useful and popular alternative source of funding for companies. This being said, like all potential sources of capital it should be carefully considered in comparison to other options.

Businesses contemplating the use of mezzanine financing should be aware that there are potentially greater costs than traditionally structured debt but also unrivaled levels of creativity when structuring the loan terms beyond what traditional banks can offer.

As such, if used with proper consideration to prevailing market conditions and risk levels it has been known to benefit both lenders and borrowers alike offering flexible solutions while minimizing onboarding requirements relative to venture capital investments.

Therefore, those seeking extension corporate financing structures may choose this route whilst deriving cost effectiveness unparallel from many of its viable counterparts.

Ryan Nead is a Managing Director of InvestNet, LLC and it’s affiliate site Acquisition.net. Ryan provides strategic insight to the team and works together with both business buyers and sellers to work toward amicable deal outcomes. Ryan resides in Texas with his wife and three children.